Related Articles

I had some readers over my house the other day, and one of them commented that she found my recommendation of You Need a Budget to be useful. She asked if I could write a little more on budgets and finance both in the context of miles and points and generally.

One thing I love to do is to gamify situations. Â Rather than feel like I’m trudging through paperwork, I like to feel like I’m trying to beat the system to achieve a certain goal. (That’s part of the reason I like couponing/deals/miles/points so much).

One “game” I’ve been playing with myself lately is a $100 per week game to try to re-center my brain financially. I’m trying to see if I can spend under $100 per week.

But first, I want to explain why I’m doing this. My financial situation has changed so much in the last decade. Ten years ago, I was in graduate school and trying to balance jobs that actually paid money (but gave me no experience towards my career) and internships that paid no money (but gave me that needed experience).

I ended up doing classes, internships, and bartending in the in between times, which made money pretty tight. I remember trying to budget out getting to go to a happy hour with a friend once in a while but found the $3.50 / drink pretty hard to swallow (get it?) when that could buy actual groceries. I turned down a lot of invitations to go out, and sometimes food shopped to get the most calories I could per dollar.

That was the more extreme side. After I started making more money, I started being able to go to happy hours more frequently, but still focused on places with cheap drinks and appetizers.

Now, I don’t have to worry so much and sometimes find myself taking short cuts that cost me a little more financially, but make things a lot easier. But I know, in the end, this money adds up to a lot more I can be saving.

I’ve started mentally comparing, let’s say, the $5 more I pay for a two-pack of conditioner through Amazon (vs. buying in the store) to the $5 I used to agonize over for a drink plus tip when going out with friends.

So to help me remember how those little amounts can add up, I’ve started playing a weekly budget game. I’ve taken all my regular bills out of the picture and am spending a few weeks trying to stick to $100 or less. This includes food, beauty products, clothing, and entertainment. (Also, things for my dog like treats, grooming, etc).

How I do it

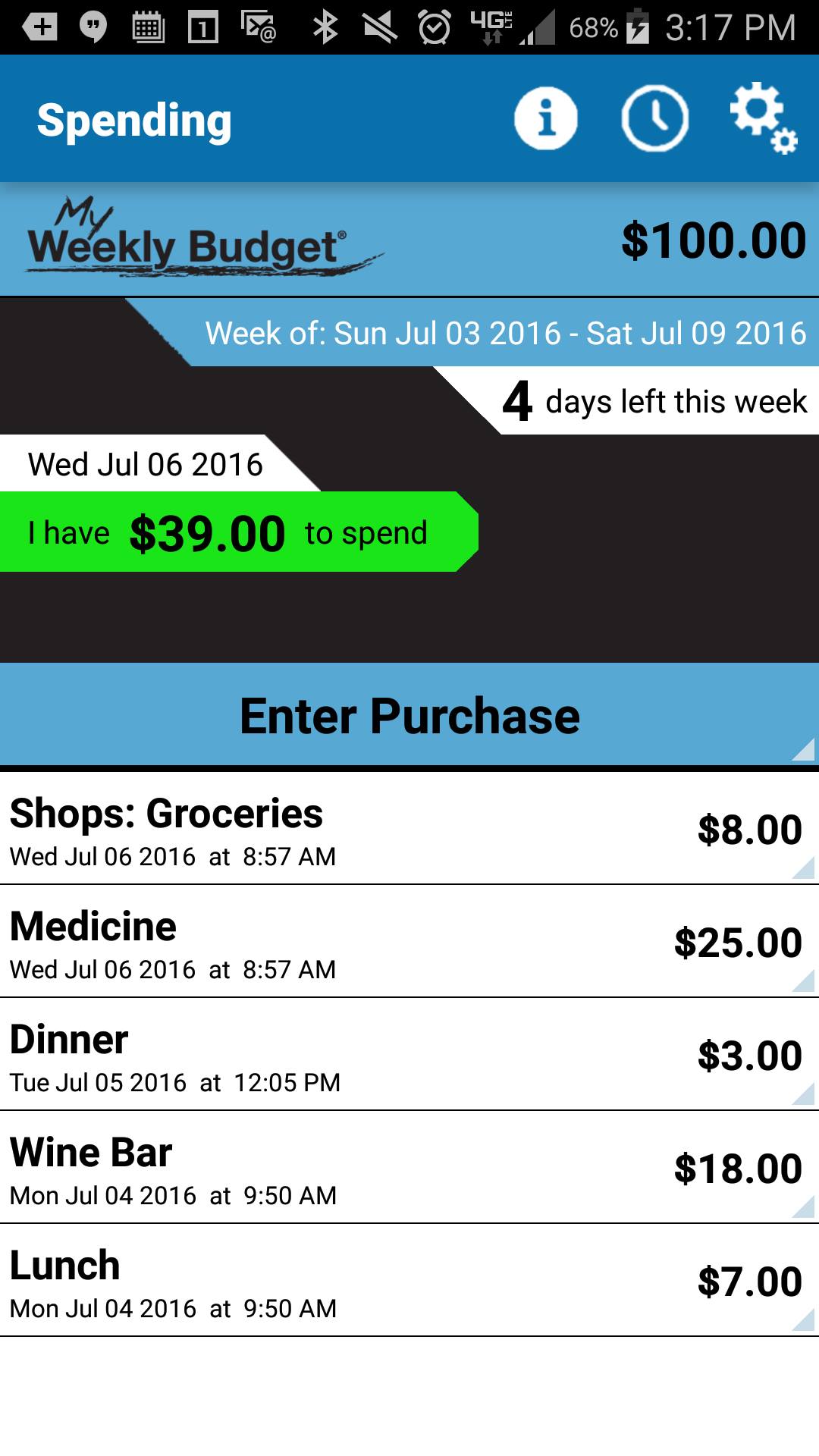

I downloaded an app called, My Weekly Budget. It was $0.99, so that was the first thing I logged into it.

I chose this app because it was totally simple. No syncing was required. No complex systems. You manually log in what you purchase, and it tells you much you have left. If you have money left at the end of the week (or went over), it asks if you want to use that to affect how much money you have.

Whenever I’ve bought anything, I’ve logged it into the system.

I allow myself a cheat. Any found money is free money. So it has encouraged me to turn in my coins and clean the house in search of more. Found food is also free food, so I’ve been eating the items that have been hiding in the back of my freezer.

I’m iffy on whether or not I should have logged my bronchitis medicine this week, but I ultimately did because that would have been a huge shock to my budget way back when.

What I learned

This experiment has definitely been enlightening for me. Â The biggest way has been through lunches.

A lot of times, I’ll forget a lunch or get too lazy to bring one and will get something delivered. That’s about $15, which would be a significant chunk of my budget. It’s made me remember more (and to get something low-cost I can use over multiple days), or run to the grocery store from my office for something cheap.

I’ll drive or metro over taking an Uber. I used to Uber when I got drinks, but now I’m also drinking less since that can eat up my budget pretty quickly.

I’m doing price-comparison shopping rather than just buying whatever Amazon has. Â For example, air filters turned out to be so much cheaper at Home Depot, but I had always been getting them from Amazon without checking anywhere else.

I’m not going to stick to $100 per week forever. Groceries add up, for example, and I’d like to eat more than just chicken, eggs, and whatever else is on sale. Plus, I did this when I wasn’t traveling, so I didn’t have to eat out.

But it’s definitely made me question a lot of my habits. I can still take an Uber, but I don’t have to take one every time. I can decide to go out during happy hour instead of later in the evening. I can stop at the store more for items instead of getting them online. I can be more frugal when it comes to lunch time dining.

The other huge cost-savings is that I got very good at doing my own manicure and pedicure. I’ll save the spa trips for a good massage when I need it, rather than hop in whenever my nails are chipped.

But I think the biggest lesson I’ve pulled from this is simple:

There’s a huge difference between $3 and $15.

I know it sounds silly, but those numbers never really felt too different. They were both “not that much”.

It has made this difference mean more to me than it had in the past. A $15 lunch is expensive, even if you can afford it. A $15 lunch affects your budget so much more than a $3 lunch does. And that $12 each time can really add up in savings.

It certainly added up in helping me hit my $100 budget each week.

Have you done anything like the $100 challenge? How did it change your shopping behaviors?

If you haven’t, would you consider doing it?

Such a great fun idea just to recalibrate financial goals! I’m always looking for new techniques to try to customize what works for me. I’m single and sometimes waste a lot of groceries. I also don’t like eating the same thing all week so I tried keeping my food budget under $10 a day so I wouldn’t feel guilty if I ate out or at the grocery store just as long as I didn’t go over $10. I’m sure $300 a month on food for one is probably a lot but I also learn that I can spend a LOT less money than I realized. You’re right those $12-$15 lunches/dinners add up!

I’ve always found that there are no cheaper calories than rice calories, no?

Yes, and this is going to sound awful but, when there was a sale on Little Debbie pies, it was about $0.15 / 1,200 calorie pie.

Awful? It sounds yummy! 🙂

Which little Debbie pie is 1,200 calories? I have to steer clear of that even at 15 cents.

It was those pies that they sell individually. They are bigger than the usual little Debbies.

This is a wonderful post from a place we don’t hear about much these days. Congratulations on your choices and skills in navigating them.

This is a pretty cool idea. I was thinking today how silly it is to be willing to spend $1 on a one-serving bag of Skittles but hesitant to spend $8 on a ten-serving package of something way healthier.

One minor quibble: what’s the opportunity cost of your time (spoiler alert: it’s pretty high)? Having it shipped by Amazon or taking Uber can be the best financial decision if it frees up time and energy you can spend blogging or doing something that will advance your career more quickly.

There’s a huge difference between $3 and $15 that DOES add up quite quickly. I struggle with this because I’m bad about putting myself in a position where the best decision is to pay for convenience when a tiny bit of thinking ahead would have saved me a few dollars and a lot of frustration.

A few days ago I bought a dozen single-serving tuna pouches to keep in my desk and take with me when I travel: http://amzn.to/2aSsVFg. I’ve gone through two of them and just asked our household COO (my wife) to add them to our subscribe-and-save list. We subscribe to these almonds, as well, and they’re nice to have in the desk. Sometimes, my lunch will consist of almonds and fruit I either bring from home or buy at the campus food court. I’ve been trying for years to improve my eating habits; this seems to be helping.

On opportunity cost, here’s a video of me growing vegetables in my office: http://artcarden.com/2016/07/12/performance-art-growing-tomatoes-in-my-office/

Here’s a summary of some of the things we’re doing to teach our kids about money:

http://artcarden.com/2016/07/25/let-kids-buy-what-they-want/

Yes to the opportunity cost, but I realized I was raising that by wanting instant gratification. So I would wait for things to add up to go to the store and go to stores that are nearby. (Home Depot is next to Target for us). I started realizing if I did a 45 minute trip to both places AND had my lists prepared ahead of time, I was valuing my time highly. If I walked to the store each time I need anything I was valuing it very low.

It great to have enough miles/points in case emergency needs pop up. The same is true (and even more so) for cash. Having enough savings to turn a personal financial emergency into just an inconvenience gives a great feeling of security.

It can surprise you how small changes in spending habits can make big changes in savings. It just takes time. In my head I always extrapolate that one weekly $15 lunch into $600+ I could save in a year (assuming still spending the $3). It can become as addictive as the points/miles hobby (or whatever you want to call it).

Churn and burn may be OK with miles, but not so much with cash.

Of course building miles/points AND cash is the best.

I live alone on a small sailboat in Mexico and my entire budget is $500. I should mention that I own my boat and am debt free and that I live on the hook to avoid marina fees. I basically come into port once every 2 weeks or so to provision and spend a weekend in town. My $500 per month budget is pretty basic: $200 for groceries/cooking fuel/lamp oil/ etc., $125 for two weekends worth of moorage at a local marina which gives me access to the dinghy dock, showers and wifi, $125 for personal spending money and $50 for the boat kitty (I try to keep this at around $500 and its for buying fuel and repairing/replacing worn-out parts). I use Mexican health care on a pay-as-you go basis (its better than you’d think and inexpensive) so I don’t carry health insurance. I should say that I have a few grand in an emergency fund to pay for major expenses like sail replacement, haul-outs and major repairs. It’s a simple life but a very good one

Just came across this thread and though old how inspiring. The more frugal I become it almost sickens me how wasteful so many people are and what they are missing out on by not living a simpler life. A sailboat in Mexico….how awesome!

Thank you for the recommendation of this app! I bought it because I am at my wits end because of my own spending habits. I spent almost $150 on food after having gone grocery shopping and having a full fridge! I am on the path to paying off my CC debt, but struggle finding the extra cash. This app will help me a ton!

I’m so glad you found it helpful! 🙂

After 3 years of seriously saving every penny that I could, I’m going to be taking 6-9 months off. No school, no work! The money I have saved will pay for my car insurance and keep a roof over my head. Otherwise, I have precisely $210 per month to spend on gas, food and entertainment for myself and my 3 year old son.

It’s not as much money as your $100/week, so I hope I can do it. I plan to walk as much as possible- and hoping my gas money won’t be needed so much.

Thanks for this inspiring post! It’s great to see someone who’s “been there, don’t that” and is surviving.

Hey Shannon,

I saw your comment and thought I’d give a bit of advice that may or may not be helpful; bike riding. because walking isn’t always practical, but cars are often not cost effective, spending a couple of bucks now on a bike, has saved me plenty in the long run, because it means frequent trips to the shops, rather than having a huge haul, and not a cent on refueling my car, as well as health benefits. other than that, the only thing I could think of suggesting would be to hoard coupons…

I am finding this hilarious, because I actually looked up this article, as a University student looking for ideas for how to stay below my weekly budget, which is, a total of $100. For a single person, groceries tend to stay below $50, per week, not accounting for eating out, my version of such usually only being $6 for single-serve Chinese takeaway… Obviously, on weeks my car needs a refill, which is hopefully rare, as I only use it once a week for my shopping trips, I’m going to spend a larger chunk of my budget on fuel over food. Furthermore, my situation is benefited by being in an unfamiliar city, therefore outings with friends are non-existent. The only problem with my system is that fresh fruit and veg do not fit into the food budget, at all. (I imagine sodium levels are a serious concern for most tertiary students living alone…) Thought I’d give the commentary of someone who’s stuck with the $100 dollars a week budget, and don’t even get me started on how skewed my budget is by textbooks…

Ella, I am not sure what town you are in but if you have an Aldi or Trader Joes near you, I often find good prices on fresh fruit and veggies there. Also, Trader Joe’s frozen fruits and veggies are budget friendly for my $100 goal as well! In Seattle, We have a few fruit/veg stands that sell “ugly” produce that is a fraction of the cost at main stream stores. Not sure if these ideas would be helpful for you!

I know this is an old post, but truly check out local farms in the area to buy produce. Google and/or facebook are a nice place to get produce fairly cheap and in small quantities. Also, if you ask your grocery store what days they put almost spoiled produce on sale you can get amazingly cheap produce and freeze it for smoothies or soups. Not quite as nice as fresh, but it still gets you really nice nutrients into your diet on a budget. Finally, buying cheap meat cuts (chicken thighs) or bones (ham bones) are inexpensive ways to get good flavor and nutrients into your diet. Chicken thighs and rice have fed me for a week before for under $8.00.

There are hundreds of thousands of people in the US who live off that much their entire lives because they are disabled and cannot work, and the Govt likes to force them to survive off $700/ month before rent!

I have had to, not played at, surviving off $100/ week or even less for years at a time before. If it weren’t possible, I would be dead. Now I could go on abt how insulting it is that it’s a game for some when we are struggling so badly, but probably no one cares because when I was homeless no one cared. When I have to go weeks eating crap food no one cares. I have no family alive. I have no credit cards and no help.

If I ever do get to where I can say now I no longer have to budget like I do, I may still budget because that way I can maybe save a couple hundred dollars? I m 43 and I have zero in the bank zero saved because I cannot save every dollar we get has to pay a bill rent or food.

Not a game for my family and I. I’m a single mother with 2 kids. I do not get government assistance. I work full time as a nursing assistant, that’s just enough to pay bills and budget $150 a week. The money that isn’t spent gets put away for the important things my kids need (school supplies, sports equipment, clothing..etc.) and for holidays. It doesn’t lead to an exciting life for me but it manages to provide the essentials we need to survive with a little extra to see my kids’ faces shine sometimes. I’ve lived worse and seeing a roof over our heads with content kids who never have to go hungry will always be enough.